Understanding Your Coverage Before You File a Claim (2026 Guide)

Replacing a roof can be one of the most expensive home improvement projects a homeowner will face. Because of the potential cost, many people wonder whether their homeowners insurance policy will help pay for a roof repair or replacement.

The answer is sometimes—but not always.

Whether insurance covers roof replacement depends on several factors, including the cause of the damage, the age of the roof, the terms of your insurance policy, and your deductible. Damage caused by sudden, unexpected events is often treated differently from normal aging or lack of maintenance.

This guide explains when homeowners insurance may cover roof replacement, common exclusions, how the claims process works, and what homeowners should know before filing a claim.

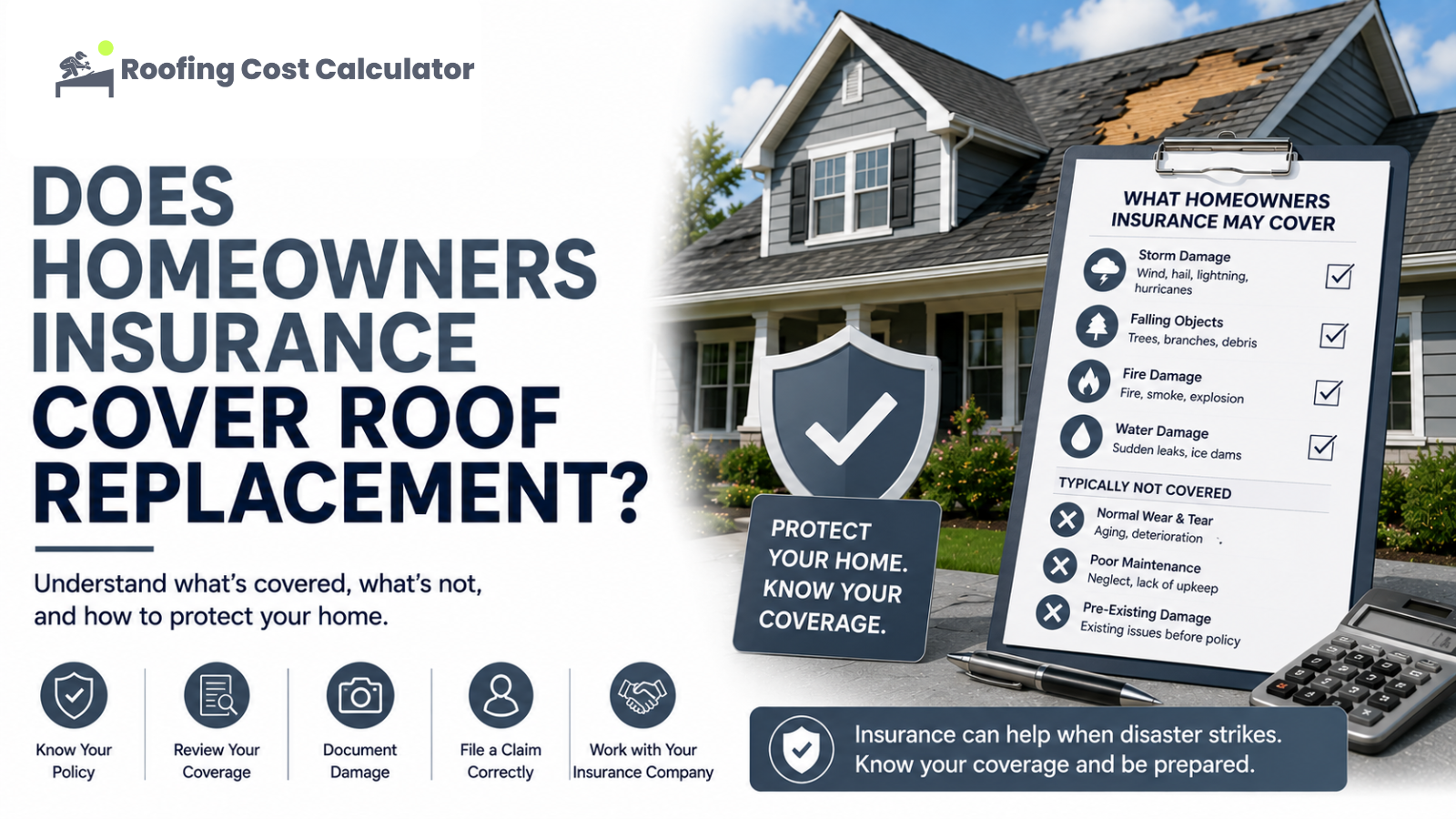

Does Homeowners Insurance Cover Roof Replacement?

In many cases, homeowners insurance may cover roof replacement if the damage results from a covered event.

Examples of covered events often include:

- Windstorms

- Hail

- Falling trees

- Fire

- Lightning

- Certain types of storm damage

Coverage varies by insurance company and policy, so homeowners should always review their policy documents or contact their insurer for specific information.

What Is Usually Not Covered?

Insurance generally does not cover roof replacement when damage results from:

- Normal aging

- Wear and tear

- Poor maintenance

- Installation defects

- Neglect

- Pest damage

- Mold caused by long-term leaks

Insurance is designed to protect against sudden, unexpected losses rather than routine maintenance or deterioration over time.

Covered Events Explained

Wind Damage

Strong winds can lift or remove shingles, damage flashing, or expose the roof deck.

If high winds from a covered storm damage your roof, your insurance policy may help pay for repairs or replacement, subject to your deductible and policy terms.

Hail Damage

Hail can crack shingles, dent metal roofing, damage flashing, and shorten the life of roofing materials.

Because hail damage is not always obvious from the ground, a professional inspection is often recommended after severe storms.

Fire Damage

Most homeowners insurance policies cover fire damage to the roof.

Depending on the extent of the damage, repairs or complete replacement may be necessary.

Falling Trees

If a healthy tree falls on your home because of a storm, insurance may cover both the structural damage and roof replacement, depending on your policy.

Roof Age Can Affect Coverage

The age of your roof may influence how your insurance company handles a claim.

Some insurers provide:

- Full replacement cost coverage for newer roofs.

- Reduced coverage for older roofs.

- Actual cash value settlements based on depreciation.

Because policies vary, it's important to understand how your insurer values your roof before damage occurs.

Replacement Cost vs. Actual Cash Value

Many policies use one of two methods when paying claims.

Replacement Cost

Replacement cost coverage generally pays the amount needed to replace the damaged roof with similar materials, subject to your deductible and policy limits.

Actual Cash Value

Actual cash value takes depreciation into account.

If your roof is older, the claim payment may be reduced to reflect its age and condition.

Understanding which type of coverage your policy provides can help you estimate potential out-of-pocket expenses.

What to Do After Roof Damage

1. Stay Safe

Avoid climbing onto the roof if conditions are unsafe.

2. Document the Damage

Take photographs of:

- Missing shingles

- Fallen branches

- Interior leaks

- Ceiling stains

- Exterior damage

Good documentation can help support your insurance claim.

3. Prevent Additional Damage

If safe to do so, take reasonable steps to prevent further water intrusion, such as covering exposed areas with a temporary tarp.

4. Contact Your Insurance Company

Report the damage as soon as practical and ask about the claims process.

5. Arrange a Professional Inspection

A qualified roofing contractor can help identify damage that may not be immediately visible.

Filing an Insurance Claim

Although every insurer follows its own procedures, the process often includes:

- Reporting the damage.

- Providing photographs and documentation.

- Scheduling an inspection.

- Receiving a claim decision.

- Completing approved repairs or replacement.

Keep copies of estimates, invoices, and communications throughout the process.

Tips Before Filing a Claim

Before submitting a claim, consider:

- The estimated repair cost.

- Your deductible.

- Whether the damage is likely covered.

- The age of your roof.

- Your policy terms.

If repair costs are only slightly higher than your deductible, filing a claim may not always be beneficial.

Preventing Future Problems

While insurance cannot prevent storms, homeowners can reduce future risks by:

- Performing regular roof inspections.

- Cleaning gutters.

- Replacing damaged shingles promptly.

- Trimming overhanging tree branches.

- Keeping maintenance records.

Well-maintained roofs are often easier to evaluate after storm damage.

Frequently Asked Questions

Does homeowners insurance always cover roof replacement?

No. Coverage depends on the cause of the damage, your policy, and any applicable exclusions.

Will insurance replace an old roof?

Not simply because it is old. Insurance generally covers sudden accidental damage rather than normal aging or deterioration.

Should I file a claim after every storm?

Not necessarily. Consider having the roof inspected first to determine whether significant covered damage has occurred.

What if only part of the roof is damaged?

Depending on the damage and your policy, insurance may pay for repairs rather than full replacement.

Can poor maintenance affect my claim?

Yes. Damage caused by neglect or lack of maintenance is often excluded from coverage.

Final Thoughts

Homeowners insurance can provide valuable financial protection when a roof is damaged by a covered event such as hail, wind, or fire. However, policies typically do not cover normal aging or poor maintenance, making regular inspections and preventative care essential.

Understanding your policy before damage occurs can help you make informed decisions and avoid unexpected surprises during the claims process.

If you're considering replacing your roof after storm damage—or simply planning for the future—use our Roofing Cost Calculator to estimate replacement costs and compare roofing options before requesting contractor quotes.